What Lies Beneath

18.10.2018 – Fine Wine Investment –

As regular readers are aware various Amphora officials are often on the road in foreign parts spreading the fine wine investment word, most recently in Dubai and Mumbai. On this trip we finally received a question we have been expecting for some time: “If this investment is in essence such a tiny proportion of my net worth, why would I take a low risk approach?”

As responsible portfolio advisers we have always been at pains to explain the risk spectrum that is available to investors in the fine wine market. Unlike, say, the commodity markets where the decision is basically the degree to which an investor may be in or out, in the stock market and the fine wine market you have the additional ability to control risk exposure through the composition of the portfolio.

As responsible portfolio advisers we have always been at pains to explain the risk spectrum that is available to investors in the fine wine market. Unlike, say, the commodity markets where the decision is basically the degree to which an investor may be in or out, in the stock market and the fine wine market you have the additional ability to control risk exposure through the composition of the portfolio.

This is part of the attraction for any investor who might have a passion for the product (certain people might have a passion for gold but it is a pretty one dimensional investment experience), but it is also crucial for anyone for whom fine wine investment is a serious diversification tool. In such a case something in the order of 10% of a wide-ranging investment portfolio may be exposed to fine wine, and for a portfolio like that the concept of risk is a vital consideration.

This changes if you are hugely wealthy, because realistically a moderate investment return even to the order of 15% compound per annum (which is almost as good as it gets in mainstream markets) is irrelevant to you if your financial exposure to wine is less than 1% of your net worth. We will never forget the retort of a wealthy Indian businessman when we proudly told him that the Liv-ex 100 30-year return is around 14% per annum: “I’m compounding 45% in my restaurant business.”

People like this aren’t interested in moderating risk, indeed the only basis on which they might get involved is if they could find spectacular returns from the market, so how do they find these? How do you get your hands on a Margaux 2015, for example?

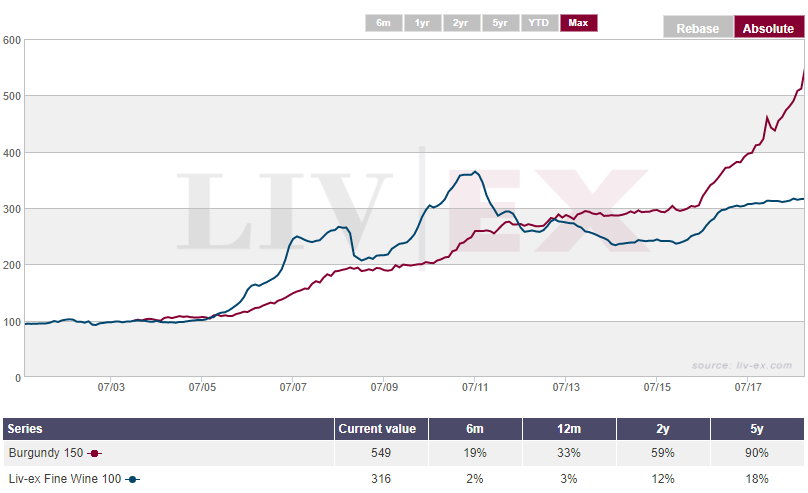

You could be forgiven for thinking that over the last 2 years the outperformance charts have been very much dominated by Burgundy, as that Liv-ex sub-index has charted one high after another.

In fact over the period since it took off in June 2016 the constituents polarise between outperformers, the DRC stable and Rousseau, and the underperformers, namely the rest. The better vintages of wines like Clos de Lambrays and Ponsot Clos Roche have tended to perform in line with the index, the “off-vintages” to underperform. Amongst the whites the better vintages have tended to outperform, the lesser to underperform.

This captures quite neatly two contrasting investment philosophies. In most portfolio investment contexts the underlying philosophy will rest somewhere in between what we might call a value style on the one hand, and a momentum style on the other. Value-based investment seeks out situations where for whatever reason the market has not appreciated how much an asset (or company) is worth. Momentum investors look for bandwagons and are happy to leap aboard.

These two styles (and the plethora in between) happily co-exist because their adoption rests on the concept of risk and the investment term. Momentum investors obviously need to be much more nimble because they don’t much like being on the bandwagon when the music stops.

This brings us back to Burgundy. It seems reasonably clear that a momentum investor will plug her/himself into as much DRC as possible and hope for the best. The “value investor” is going to take one look at the chart, however, and look elsewhere. (Apostrophes used because obviously the use of “value” in this context has no “intrinsic” connotations.)

So what do value investors do at this point? If it were any other sector we at Amphora would be looking to the algorithm for support, and the algorithm certainly highlights the best relative value across the Burgundy board. The problem the value investor has is that even the worst-performing DRC vintage from this century is up 40% over the last 2 years, so to some extent the horse has already bolted.

So what do value investors do at this point? If it were any other sector we at Amphora would be looking to the algorithm for support, and the algorithm certainly highlights the best relative value across the Burgundy board. The problem the value investor has is that even the worst-performing DRC vintage from this century is up 40% over the last 2 years, so to some extent the horse has already bolted.

Que faire? The answer may lie in comparing the performance of all the DRC wines over that time frame, and what is revealed is that the cheapest (in absolute value terms) have all performed better than the most expensive. In other words, the best return from a Romanee Conti is 115% over the period under review, whilst for the “lesser lights” the numbers read: Echezeaux: 159%; Richebourg: 250%; Saint-Vivant: 265%; Tache: 186%.

This suggests that there has been a deceleration in the rate of price appreciation at the more expensive end of the market, and this shouldn’t come as too much of a surprise. The more rarefied prices get, the fewer people there are to pay up, and those who do want to get involved move down the quality chain.

This of course begs the question: what lies beneath the above names in this “quality chain”, and the answer lies in all those components of the Burgundy sub-index, and others outside the index by the way, whose prices are yet to take off. The question therefore becomes, if Romanee Conti affiliate wine prices have been dragged up by the top Grand Cru itself, when does the fervour spread to the rest of the sector?

Our sense is that the very scarcity of most Burgundy names is likely to keep the ball rolling, barring some cataclysm in the global economy, so we would be very happy to help investors who might choose to focus on this vibrant part of the market.