Stop: correlate and listen

21.02.18 – Wine investment –

It is always interesting when stock markets have a wobbler, even if it is uncomfortable at the time. The fact is that the closer you are to the action, the worse everything seems to be. Most people remain blissfully ignorant of equity and bond market gyrations, even though through pension funds we are all pretty much exposed. The media loves nothing more than a good shake out, of course. When the Dow Jones Industrial Average had its worst week in 2 years recently it was headline news. Last week’s rebound which was the best performance in 5 years barely merited a mention. “If It bleeds, it leads.”

At times of crisis investors cast around for alternatives and often physical assets come into focus, because they are perceived to have some mystical inherent value. The problem is, this “value” is as subject to market forces as the collective view of how well management at HSBC, for example, might be doing. Notwithstanding, it is possible to gauge these swings from one asset class to another through the use of correlation charts.

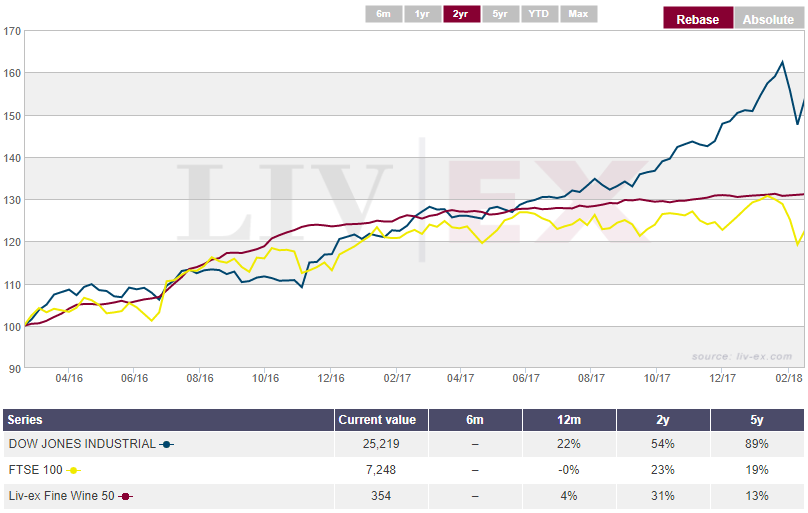

The above chart illustrates the degrees of correlation between The Dow Jones IA and the Liv-ex 100 (the red line), the FTSE and the Liv-ex 100 (the blue line), and the gold price and the Liv-ex 100 (the green line). When the indices are preforming together in lock-step, as it were, the line moves towards 1.00. When they are moving in opposite directions, the line moves towards -1.00 (1.00). (Please note that the data only stretches to June 2017.)

As we can see, there are times when the indices move together, and times when they don’t. The chart doesn’t specify whether this happens to be up or down, incidentally. The red and blue lines harmoniously spending the last 12 months somewhere near the top of the chart just mean that they are moving for that period in the same direction, not that they are flat over that period, or indeed either moving up or down. Simply the same direction.

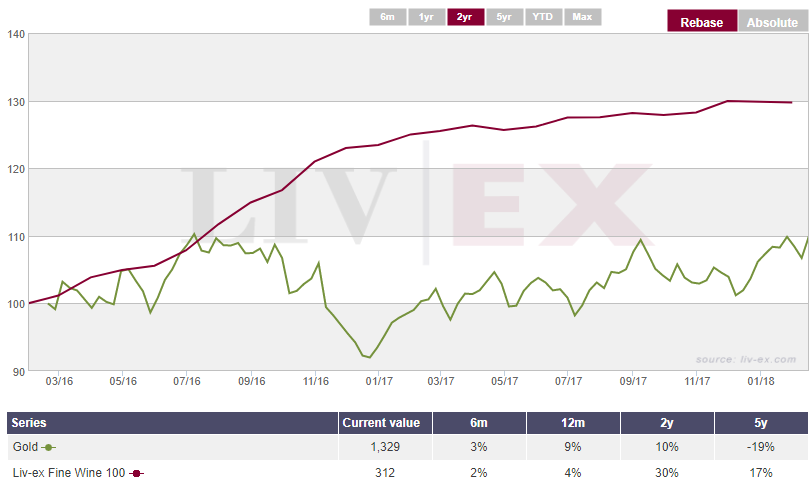

Equally, the gold price quite clearly disengages from the Liv-ex 100 in the second half of 2016. Here it is doing so, in relative terms:

What asset allocators try and achieve in the investment process, is maximum exposure at times of outperformance, and minimum at times of underperformance, and in doing so they have to keep a close eye on correlations. If an asset correlates closely with the equity market, for example, an investor might just as well own that asset instead of (or as well as) a portfolio of equities, when he/she feels positive about equities. In addition you can under-own or short such an asset for hedging purposes.

This gets complicated, of course, when a correlation disappears; an investor needs to be alert to these swings, and understand why they happen. What makes life difficult is if there are no discernible patterns, and we think it unarguable that over the last decade there are far more discernible patterns between equity markets and fine wine than between either of them and the price of gold.

From a low point (i.e. an uncorrelated phase) between mid 2015 and 2016, the fine wine and equity market indices have marched to the same tune, much as they did in 2009. In Q2 2010 the equity markets had their first correction after the initial recovery from the woes of the financial crisis, whilst fine wine prices motored ahead. That ended a lengthy period of correlation.

The correlation between fine wine and the FTSE was still intact until very recently, whilst with the Dow it has broken down somewhat over the last few months, as the Dow initially out, then under-performed:

There is a significant constituency expecting the current bond yield rises to spell an end to the bull run in the US equity markets, with consequences rippling throughout the rest of the world. Whilst that is not the Amphora base case view, if it does happen the current stability in the fine wine market is going to look increasingly attractive. In our view either equities slide for a stretch, and the correlation with fine wine moves back towards -0.1, or they recover, and the correlation remains intact. Either way is good for fine wine prices.

Meanwhile the Year of the Dog is upon us, the first “Earth Dog” since 1958, for what that’s worth. The Chinese will be emerging from their annual holiday later this week and it will be interesting to see how their markets respond to what has happened since they went away.

We note with interest that a good number of late 20th century vintages have started this year buoyantly, and wonder if this is because they are starting to diminish in supply now that they are so well into their drinking window. We have long argued that the potentially dramatic increase in consumption from the developing markets is not yet discounted in fine wine prices. Perhaps this is also an expression of that.