Latour 2005 ex-chateau release

14.03.2017

A propos the forthcoming ex-chateau release of the next tranche of Latour 2005, the Liv-ex blog at the end of last week carried a chart of the last 10 physical Latour vintages with the conclusion that “Parker points become increasingly valuable for higher vintages”. I am not sure whether this quite gets to the heart of the matter, from an investment perspective. We all know that 100 pointers seem to merit a premium, rather as do most Millennium vintages. We also know that we had a 2005 retrospective two years ago and wonder what that vintage will do for an encore?

Wine prices, in the same way as stocks and shares, move on surprises. When a listed company starts doing better than the market expected, its share price will outperform. When Robert Parker raises his score from 98 to 100, the price of the wine receives a lovely shot in the arm. When the UK votes for Brexit and everything becomes 10% cheaper for a foreign buyer, the prices respond accordingly.

So what is new in respect of Latour 2005 that forces a reappraisal of our view? Oh hello! More supply to the market! Now at Amphora we never tire of luxuriating in the fabulous supply/demand dynamic that the fine wine market enjoys, but this is predicated on supply diminishing, as it ultimately does, no matter how many ex-chateau releases Latour indulge in.

Latour seems to pride itself however on keeping everything from production levels to size of each tranche that they release to the market an absolute mystery, and this certainly should not raise the comfort level of a potential investor.

There is always a step into the unknown to some degree when making an investment. Will management do what they said they would, for example? It is the same with the fine wine market. You assess what you think you know, and take it from there. When what you think you know is that the supply/demand dynamic will temporarily be derailed by a flood of new supply you avoid it like the plague, would be our advice.

There is though a single straw for Latour 2005 bulls to cling on to. It has underperformed so badly against most of its sister wines that it may be coiled for a spring. Here it is against the 2002 which is worth using as a lower scoring back vintage, and therefore unlikely to see any ex chateau releases in the future. The Liv-ex blog mentioned above sees the 2002 as being undervalued, but it posts the Wine Advocate score at 96. If you use Lisa Perroti Brown’s 2012 Wine Advocate score of 94 it no longer is undervalued, but that’s another story.

Any bull argument for the 2005 has to be predicated on the fact that, not only is it poised after its underperformance, but this new supply we are about to get is the REASON for the underperformance, and once out of the way is an uncertainty removed, and is therefore a good thing.

It is instructive at this point to look at what happened to other ex-chateau releases in recent times. Almost exactly 2 years ago Latour released a tranche of the 2003, and last year at this time a tranche of the 2000. The 2003 is a perfect 100 pointer, and the 2000 is obviously the Millennium vintage, and scores 99. In both cases you could have been as excused for buying as you now could be for the 2005.

Let’s have a look at both alongside the aforementioned 2002, firstly the 2003. This chart like the one above rebases both to the starting point, in this case the moment 2 years ago when the tranche of 2003 was released.

Quite clearly the market did not buy into the idea that there was no more 2003 still up the Latour sleeve. In stock market parlance this is called a “tap”. If the market believes a big shareholder is dribbling stock out into the market it creates a headwind against which it is very difficult for the share to perform.

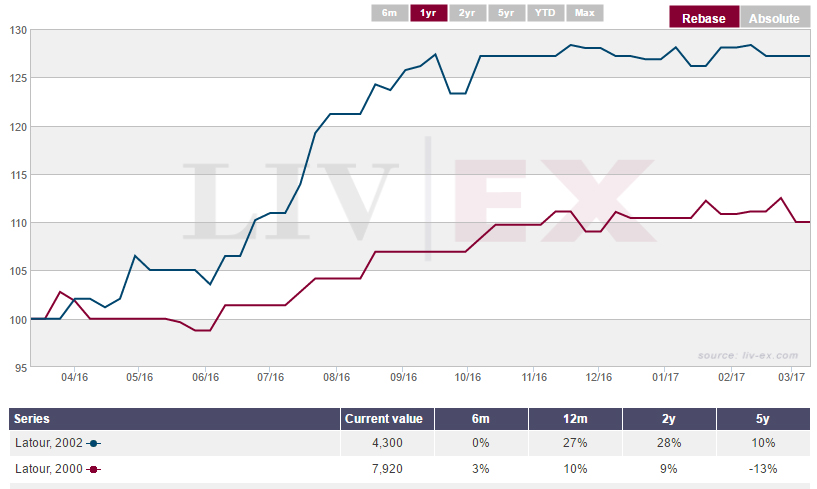

And what of the 2000, on this occasion rebased to release a year ago?

The message is pretty clear. The market doesn’t trust Latour to have no stock left to release, or at least it certainly didn’t in the immediate aftermath of the releases. Some might argue that after a period of underperformance the above on vintages are due to outperform. This entirely misses the point. Wines don’t start to outperform because “it is their turn”. They do so for a reason.

A lot of air will be expended on the release price of the forthcoming 2005, judged against the current market price. Typically the chateau will get some credit for releasing AT the current market price, because they have had a habit in the past of listing at a premium, on the altogether spurious grounds that ex-chateau wine is of even more perfect provenance than the already perfect provenance of wine that has never left the UK bonded system.

Amphora believes this is nonsense in investment terms. Latour 2005 is not a great buy at the current market price, taking all relative value arguments into consideration. It is an even worse buy given the weight of new supply. Subscribe for the new issue by all means, but not if you are trying to make your money grow.