Lafite’s looking lucrative

22.08.2018 – Fine Wine Investment –

Earlier in the month we looked at the ongoing popularity of Lafite as expressed by its dominance of trading platforms and search engines, and noted the curiosity of this, juxtaposed against the underperformance of First Growths against the broader market. We constantly read that Bordeaux’s market share on Liv-ex is in decline, and when you see that The Liv-ex 50 has lagged the broader Liv-ex 500 index, comprising the full spectrum of Bordeaux wines even including Sauternes, you get an impression of how out of favour First Growths seem to be.

On a 2 year view the Liv-ex 50 (all 5 First Growths’ last 10 physical vintages) has risen by 14%, the Liv-ex Bordeaux 500 (last 10 physical vintages of 50 producers from every part of the region) has risen by 19%, whilst the “Fine Wine 1000” which takes a fully global perspective is up by 27%. So the global index has outperformed the First Growths over a mere 2 years by the best part of 100%.

It is of course entirely possible that the frequency of platform visits for First Growths may result from the fact that these are most widely held and the visitors were simply looking to offload rather than purchase, but that doesn’t really wash when you take Mouton 2000 into account. This “collector’s piece” is the best performing Mouton this year having risen 15%, but trades at the extraordinarily high price of £20,000.

It is of course entirely possible that the frequency of platform visits for First Growths may result from the fact that these are most widely held and the visitors were simply looking to offload rather than purchase, but that doesn’t really wash when you take Mouton 2000 into account. This “collector’s piece” is the best performing Mouton this year having risen 15%, but trades at the extraordinarily high price of £20,000.

At Amphora we never tire of saying that everything is relative, and if you lived in a DRC bubble you could be excused for thinking that £20,000 for 12 bottles of something is really rather cheap, but of course for a Mouton it is off-the-scale expensive. That hasn’t stopped it being not only the best-performing Mouton Rothschild year to date, but also the best-performing First Growth.

When you analyse the Liv-ex 50 constituents’ individual performances over the 2 year time frame referred to earlier, the First Growth story becomes more interesting, because there are very clear winners and losers. In efficient markets there are always winners and losers, but mis-pricings are eradicated pretty quickly. As you move off the mainstream inefficiencies creep in, revealing prices which sit around at the wrong level for long enough to allow the savvy investor to take advantage.

Remember that the Fine Wine 1000 is up by 27% in the period under review, and that a First Growth doing as well as the Bordeaux 500 which is up 19% would have outperformed its peers quite considerably. Taking as our control sample only physical vintages from 2000 and after, only Lafite and Mouton offer vintages which are up over 27%, whilst between Latour and Margaux there is only the Margaux 2014 which is up over 19%. Haut Brion has 2 over 19% and none over 27%.

By contrast, Lafite has 7 vintages which have outperformed the Bordeaux 500, and Mouton has 5 outperformers and a further 7 which are in line. This means that if you have owned something with Rothschild in the name over the last 2 years your chances of doing well have improved considerably. Between Lafite and Mouton, 5 in total have even outperformed the Fine Wine 1000, and they make for interesting reading.

Consider for a second the fact that we are looking at the period from August 2016. At that date the broad market having bottomed at the end of 2015 is roughly half way through its rally to current levels, and the 2013 vintage has just become physical. Of these 5 outperformers, one is the unstoppable Mouton 2000 (+33%), but the 3 Lafites are 2014 (+40%), 2013 (+33%), and 2012 (+28%).

What this is telling us is that the market in the earlier part of the rally was reluctant to believe that any of the post 2009 and 2010 en primeurs could represent good value, because the scars of the “post-crash” phase were still raw. Everyone had been conditioned by the narrative that they were all still being badly priced, and that much of it had been left in the warehouses of the negociants in Bordeaux. In the parlance of a stock market IPO, they were soiled goods having been “left with the underwriters”.

As you work your way through a rally, however, the narrative evolves, and belief sets in. People cast around for things which seem to be too cheap, and before you know it even these former dogs begin to develop a price momentum all of their own, but then you need some idea of when enough is enough. Do I sell my Lafites 2012, 2013 and 2014 just because they have done well, or hold on because they have such good momentum?

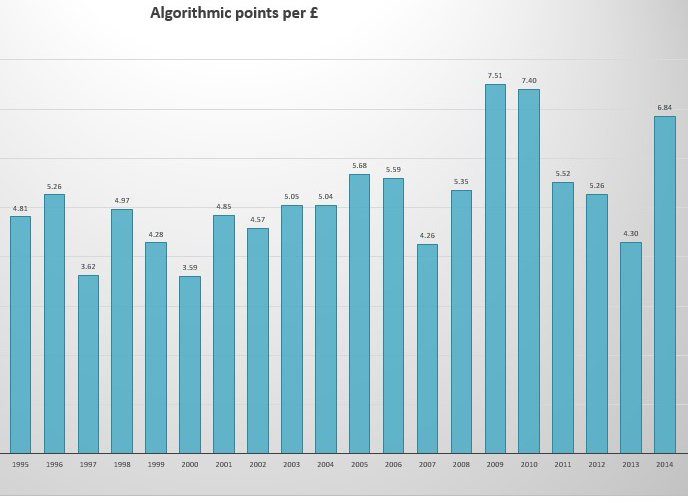

In a vacuum the answer is just a wet finger in the wind, but regular readers will not be too surprised, we hope, to now be confronted with this:

Our 3 friends are all close to £5,000 per case, although the 2014 is marginally the most expensive, and the 2013 marginally the least. Taking into account all the variables against which wines are priced, which is precisely what the algorithm does, we see that in fact the 2014 is still very much a buy despite its recent performance, whilst the smart move would now be to offload the 2012 and the 2013.

Our 3 friends are all close to £5,000 per case, although the 2014 is marginally the most expensive, and the 2013 marginally the least. Taking into account all the variables against which wines are priced, which is precisely what the algorithm does, we see that in fact the 2014 is still very much a buy despite its recent performance, whilst the smart move would now be to offload the 2012 and the 2013.

We have spoken in the past about the great value resident in the 2009 and 2010, manifest in the table above, and given what we are seeing about Lafite performance in the broader market it simply doesn’t stack up to avoid them because of some perception that buyers have some sort of downer on First Growths.

At present the market prices older Lafite “off-vintages” around £6,500, newer “off-vintages” around £5,000, the RP 100 pointers of 1996 and 2003 around £9,500. (Neal Martin, incidentally, doesn’t rate these at 100 but the market seems to agree with Robert Parker for the moment.) It prices the 2008, 2009 and 2010 around the £7,500 mark. If this is correct then there are some incredibly good value 2008s around, but to rank 2008 alongside 2009 and 2010 seems to fly in the face of accepted wisdom. The Parker overall vintage scores for Pauillac from 2008 through to 2010 respectively are 91, 99 and 98. 2008 is simply not in the same bracket.

We noted earlier that the market narrative can sometimes go awry, and when it does there are things for the active investor to do. The narrative in respect of these top Lafites is demonstrably wrong, leaving a golden opportunity. Picking up Lafite 2009 and 2010 at these levels will from some point in the future look like an inspired decision. These are the 1982s and 1986s of future generations.

We repeat: buy Lafite 2009 and 2010.