Know your quarry!

It is of great interest to us at Amphora that not only do certain noisy people deride fine wine investments as an investment asset class, but others seem happy to participate without doing what they’d do for any other material financial outlay: find out a bit about the market and how it operates before laying down their money.

The fact of the matter is that wines don’t all rise and fall in price at the same time. And even if you take a very long term view of things, you can’t escape the likelihood of underperformance if you don’t pay attention to what you are doing. The art of long term investing revolves around the beauty of compounding growth, but the reverse is also true unfortunately. If you compound an underperformance, your returns will steadily worsen over time.

Fine wine investments analysis

This week, we analysed the performance of individual wines since the market bottomed at the beginning of December 2015. This is actually quite an important time, judging by the performance of the Liv-ex 50, the market hadn’t touched that level since early 2010. We were therefore coming off a huge rise, a thorough shake-out, and a lengthy consolidation.

We also removed wines over 20 years old from the study. From that point, liquidity tends to diminish and prices become more volatile.

This is even seen in our current research with certain wines from the end of the 90s. So where necessary, we’ve ignored these as outliers. Just to be clear, there is absolutely nothing wrong with buying older wines for either investment or, obviously, consumption – but they tend not to be so easily accommodated within the construct of a fine wine investments portfolio.

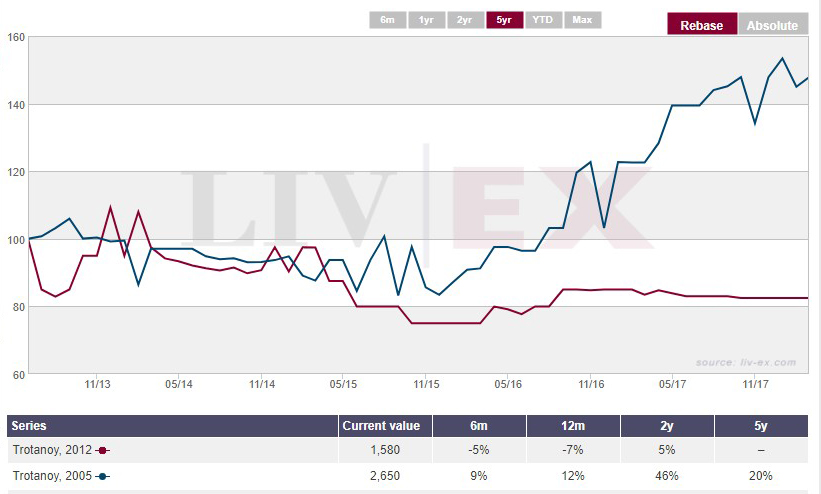

The performance range of vintages from all producers is extremely wide over the period under consideration (28 months). One of the wider spreads is exhibited by Trotanoy. If you had bought the 2012 at the start of the term, you would have made around 5 per cent, whereas the 2006 would have appreciated around 70 per cent. Here is the chart illustrating this divergence:

Note the timeline at the bottom. This is a 5 year view, but the 2005 really starts to escalate as the market turns north at the end of 2015, the 2012 having become physical earlier that year.

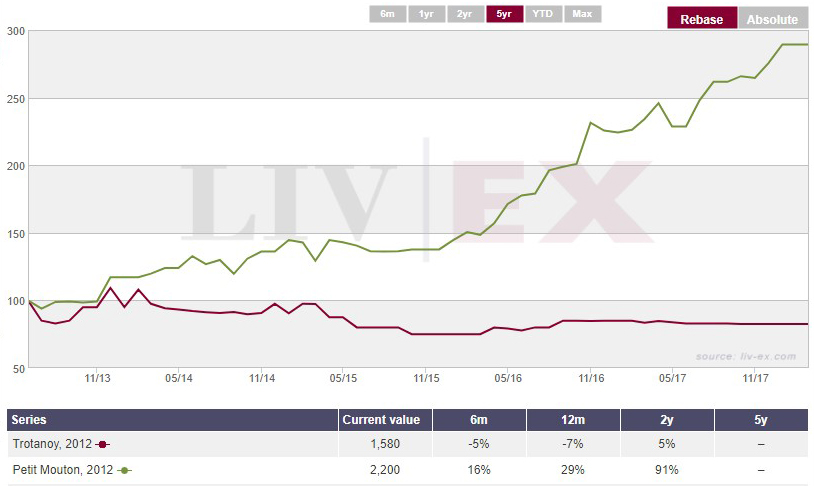

Not that there was anything wrong with the 2012s in general at this point. Far from it. Imagine if someone had suggested you buy Petit Mouton 2012 instead of Trotanoy 2012. Here is the chart over the same time frame as earlier:

Against the Trotanoy’s 5 per cent, the Petit Mouton would have gone up 120 per cent. That’s the sort of steer most people should be looking for, in our view!

Las Cases and Barton

Certain wines have a somewhat smaller spread, but even the narrowest is still a healthy 25 per cent. Leovilles Las Cases and Barton represent a particularly interesting study in this respect, because whilst in both cases the spread is the same, they are respectively bookended by the opposite wine.

Leoville Las cases’ “poorest performer” (excluding outliers) is the 2007, rising just 24 per cent whilst the 2013 rose 51 per cent. By contrast, Leoville Barton’s best performer is the 2007, up 53 per cent, whilst its poorest is the 2013, up 25 per cent.

The key question, of course, is how could we have known that the best LLC might have been the 2013? The answer is that you couldn’t because you don’t have a crystal ball. Fortunately, investing is not about looking into crystal balls, it is all about playing the percentages, and it will come as no surprise to regular readers to learn that this is precisely where the Amphora proprietary algorithm comes in.

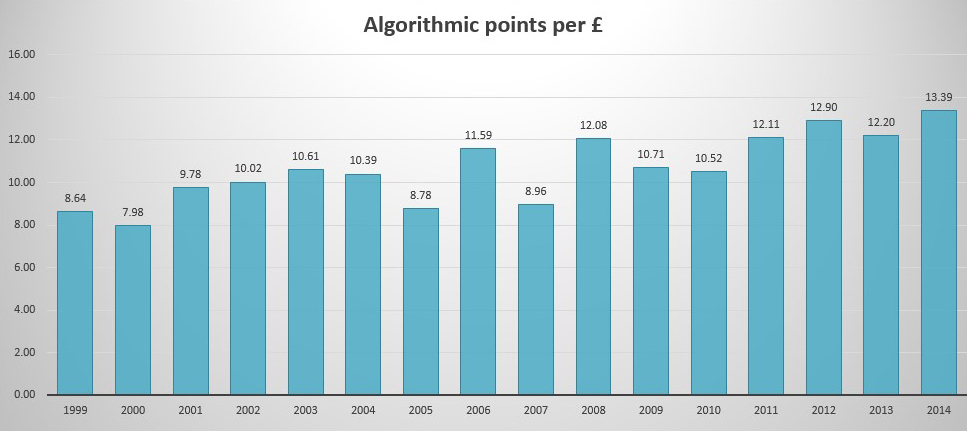

Here is the algorithm at work, in respect of Leoville Las Cases:

Here, the prices have been backdated to the beginning of December 2015, to see what the algorithm would have encouraged us to recommend at the time. Remember that the higher the column, the more you are getting for your pound, so the top 3 picks would have been 2012, 2013 and 2014. Equally, the bottom 3 would have been 2000, 2005 and 2007.

If you had invested equally in the ‘top’ 3, your aggregate return would have been 42 per cent, whilst the ‘bottom’ 3 would have risen by 25 per cent. Don’t be deceived by the 25 per cent into thinking that you would have done well. You wouldn’t. You would have underperformed the top picks by a spectacular 70 per cent, over less than 30 months.

The wine investment market

This is precisely what we referred to earlier. Even a gibbon could make you money if the overall market was going up, but it is the degree of return which is key here. At times of both feast and famine, an investor’s goal should be to maximise returns, because the objective is to make a small amount of money into a large amount without an undue level of risk.

There are metrics available in mainstream markets to help understand and analyse value, and it’s fundamental value for the most part at that. Many of the assets sweat dividends. In a market place absent of dividend discount models, an investor needs help to separate the wheat from the chaff. As illustrated above, the algorithm is a great tool for unearthing relative value and conjuring significantly enhanced returns.

And if you want to make good use of it when you invest in fine wine, take a look at our fine wine investments services.