Calm conditions

23.04.2019 – Fine wine investment –

You could be forgiven for thinking that the fine wine market has quite gone to sleep this year, so marginal do the index movements seem to be. It is unusual for us to be awaiting the en primeur campaign with such great excitement, but something is needed to stimulate the senses! There are high hopes for 2018 and as ever the devil will be in the pricing, but at least investors won’t be able to ignore it.

So, are the somnolent indices hiding any subcutaneous activity that we should be bringing to your attention? What tends to happen during periods of relatively low activity is that prices get distorted by the lack of liquidity, so it doesn’t make so much sense to highlight the fact that Dujac Clos de la Roche 2014, for example, seems to have fallen 47% this year. In reality, it hasn’t.

The Liv-ex market price for a case of 12 was round about £6,000 on January 1st this year and it is now £3,168. The trouble is we defy anyone to be able to pick up a case for that figure, the majority of market availability being just north of £5,000. Distortions are a fact of fine wine market life and you have to look behind the advertised numbers much of the time to see where the real market is, especially when things are quiet.

There tends to be better liquidity in Bordeaux, of course, so we have analysed the performance of over 30 of the most traded names to see if anything interesting is happening under the bonnet. This examination has looked at the performance of all vintages since (and including) 2000 and as ever the results are quite revealing.

For the most part you could throw a handkerchief over the range of price movements. All Angelus wines, for example, have moved between a range of a rise of 3.69% (2009) to a decline of 5.88% (2003), resulting in an average movement of 0.09% and a cumulative movement of +1.47%. The Lafite averages are even flatter, between a range of +5% for the 2004 and -4% for the 2000. Its aggregate of price moves is zero!

14 producers, however, exhibit a much wider range of price movement, curiously split between 7 that have risen by more than 20% in aggregate terms, and 7 that have fallen by over 20% on the same basis. There is life in the undergrowth after all! There is no great right bank/left bank bias going on either. Risers comprise 4 Left Banks and 3 Right Banks, as do fallers.

Clearly any aggregate or average calculations can be influenced by outliers, as seems to be the case with Lafleur 2008. On the face of it Lafleur 2008 is up 31% this year, but in fact the reported market price here seems to be anomalous. Last week it was quoted at £6,320 yet is available in the market at around £5,500. Sometimes an anomaly can skew the market price and this highlights the requirement to cross check all data before coming to any conclusions, and certainly before going to market. Obviously this is precisely what we at Amphora take great pains to do.

Even allowing for a price of £5,500 Lafleur has done quite well this year, but not so noticeably so. Unlike, say, Vieux Chateau Certain. VCC has managed an aggregate rise of 43% across all its vintages (since and including 2000), despite having a best performer rising only 14%. This suggests of course that as a house VCC has been quite a popular target in 2019.

Moving onto the Left Bank, the Pichons Baron and Lalande find themselves in this category. In each case the best riser is only high single digit, but there are far more risers than fallers, so the aggregate is not compromised by a welter of fallers. Again this suggests that there has been a reasonable degree of interest across the board for these chateaux.

On the other side of the coin, the second wines of Lafite and Latour have come in for a bit of stick year to date. Again the absence of outliers leads to the conclusion that there has been a degree of genuine selling of Carruades and Forts, as there has been for Mission Haut Brion, whose statistics would suggest it has been particularly unloved this year. Apart from the 2004 (+1.52%) and the 2002 (+1.27%), and the 2013 which is unchanged, every single other vintage has declined.

Over in St Emilion we find that Cheval Blanc has fared even worse. Three vintages are unchanged, the 2005 is up £50 to £6,800, but everything else has declined. The worst performer is the 2002, down 10.53%, and we point this out because in fully 25% of the studied wines, the 2002 was the worst performer.

There is a good cross-section of Bordeaux society in this study of 32 producers, so to find quite such a preponderance (8) is noteworthy. There are 3 from 2012 and 3 from 2014, so the 2002s have been singled out for selling pressure. At this point there are no great conclusions to draw from this; both sides of the river achieved indifferent regional vintage scores in 2002, and no 2002s show up well on the Amphora algorithm, so it may just be a case of market drift affecting them disproportionately.

Either way until and unless they drift significantly lower we will not be recommending buying them. That said, a particularly eminent critic approached one of our Asian partners in 67 Pall Mall bearing a glass of Montrose 2002 and told him that the market had got it all wrong and the 2002s were the best thing since sliced bread! Well as we all know, it takes 2 views to make a market.

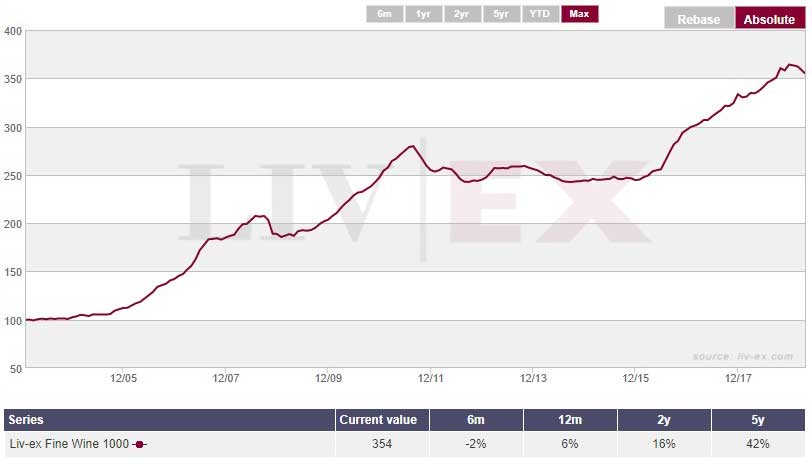

We reiterate that it is hardly unusual for markets to engage in a quiet spell after a good rally, and this, after all, is what the Liv-ex 1000 has just done:

Any coherent investment adviser will tell you that occasional pull-backs are healthy – nothing sustainable goes up in a straight line. Arguably the only unusual thing about the last few months has been the lack of newsflow, and maybe most people have had so much glued to the Brexit scenario that other news has paled into significance. Well here comes 2018 en primeur, with a fabulous opportunity to arouse the giant!